Tags

Brexit, China, decoupling, European Union, Eurozone, Financial Times, France, Germany, IMF, International Monetary Fund, United Kingdom, {What's Left of) Our Economy

Some awfully interesting evidence supporting my view (see, e.g., here) that the United States is uniquely positioned in the world to prosper quite nicely from seeking to maximize its already high degree of economic self-sufficiency has just emerged — and from some awfully unlikely sources.

It’s indirect evidence, to be sure, and concerns the United Kingdom’s (UK) economic perfomance since the Brexit referendum of 2016 that mandated its pull-out from the European Union. But it’s relevant to the United States’ situation because the U.S. economy is far more actually and potentially self-sufficient.

The evidence – from the ardently globalist International Monetary Fund (IMF) and from the just-as-ardently anti-Brexit Financial Times – makes clear that since the UK finally left the EU at the end of January, 2020, it’s gross domestic product (GDP – the standard measure of a national economy’s size), has not only risen about as fast as those of the major members of the EU, but that it’s closed the gap that existed pre-withdrawal. And all the while, the UK has reaped a crucial benefit – much more control over its future.

The IMF evidence came in today’s release of its World Economic Outlook – a twice yearly Fund publication that surveys the state of the globe and includes growth forecasts for major countries, geographic regions, and formal groupings of countries like the eurozone (which overlaps pretty thoroughly with the EU).

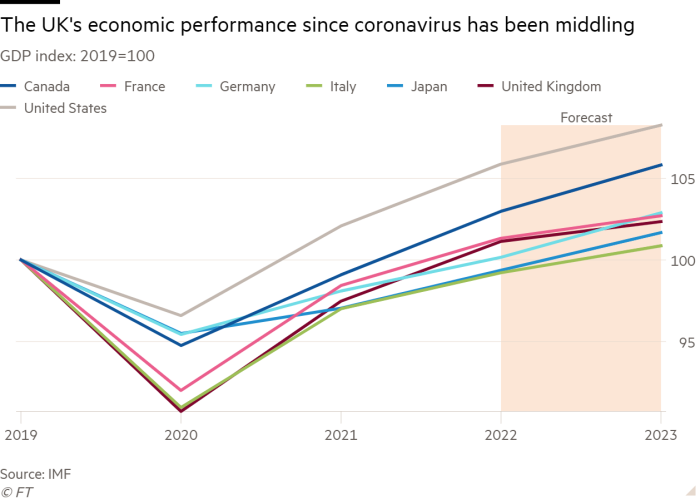

According to the Fund, last year, the UK economy expanded by 7.4 percent in inflation-adjusted terms (the most closely monitored gauge of growth). The figure for the countries using the euro as their currency? A mere 5.4 percent. And it’s not like the lagging eurozone performance was dragged down by its long-time economic laggards. Germany’s real 2021 growth was a measly 2.8 percent, and France’s much better seven percent still trailed the UK’s.

In other words, a single country that’s cut itself off from all the alleged benefits of economic integration with a much larger market had out-grown the collective members of that market that presumably were enjoying all the economic advantages of such integration.

Moreover, the IMF’s latest projection for this year crowns the UK as a growth winner, too. Its 2022 price-adjusted GDP is forecast to improve by 3.7 percent, versus 2.8 percent for the euro area. The French after-inflation growth rate is expected to top the UK’s slightly (2.9 percent), but Germany’s will be stuck at a lowly 2.1 percent.

The only solace Brexit-haters can take from the IMF analysis is that the UK supposedly will fall way behind growth-wise next year. Its real GDP performance is pegged at a mere 1.2 percent – slower than that of the euro area (2.3 percent), France (a not-so-impressive 1.4 percent), and Germany (a respectable 2.7 percent, but a performance coming off an unusually low baseline). Yet needless to say, it’s much more reasonable to put more stock in near-term predictions and longer-term predictions.

In addition, even with this possible slowdown, the Financial Times graph below (taken from this article) shows that, despite its glass-half-empty title, if the IMF is right about 2022, the UK will have turned itself from a growth laggard in 2019 compared with France and Germany to a growth equal. And although the 2023 projections are tough to see in this graphic, they show near parity among the three.

Two qualifications to these findings need to be made. First, as I’ve repeatedly noted, all economic data for the last few years has been dramatically affected and surely distorted by the CCP Virus pandemic. Second, although the UK left the EU, it still does business with the bloc and its economic ties with the rest of the world stayed the same organizationally.

At the same time, for years after the referendum vote, businesses in the UK had been dealing with major uncertainties and the inevitable short-term costs of the negotiations over Brexit’s precise withdrawal procedures and terms. And the growth figures make obvious that, on the whole, they and the entire economy have managed to navigate them successfully.

And if the UK has so far emerged successfully from its Brexit-style decoupling from the EU, it’s hard to imagine that the much more economically diverse United States can’t emerge from a much more determined decoupling from China – which will promote vital and intertwined economic and national security interests – at least as well.